Издатель

You’ve been told you’re borrowing your own money when you take a policy loan. That’s not what the contract says.

There is a ton of confusion around policy loans in whole life insurance. People are told, ‘You’re borrowing your own money,’ or ‘The insurance company will steal your cash value.’

Let’s cut through the sales talk and look at what’s actually happening in the contract, and what it means for your family and your estate.”

Disclaimer:

“This Is Not Legal Advice, For Education Only”

First, a policy loan is not a personal IOU or borrowing your own cash.

It’s a loan from the insurance company, with your policy’s cash value as collateral.

Think of your cash value as the equity in a house. You don’t rip the bricks out of the house to get money; you borrow against the equity, and the house stays standing.

Same idea here: your cash value stays in the policy, continues to earn its guaranteed growth and potential dividends, and the company advances you their money, secured by that cash value.

Now, the part most people never hear clearly: interest and collateral.

When you take a policy loan, the insurance company charges a stated interest rate. That interest doesn’t come out of thin air; it accrues on the loan balance, just like any other loan.

If you never repay it during your lifetime, the company doesn’t chase your kids. They simply subtract the outstanding loan plus interest from your death benefit before it’s paid to your beneficiaries.

From an estate planning perspective, that means two things:

1. You’re effectively choosing to ‘repay’ the loan with a reduced death benefit if you don’t repay it during life.

2. As long as the policy is monitored and doesn’t lapse, your heirs still receive what’s left—net of the loan—without going through probate.”

Visuals:

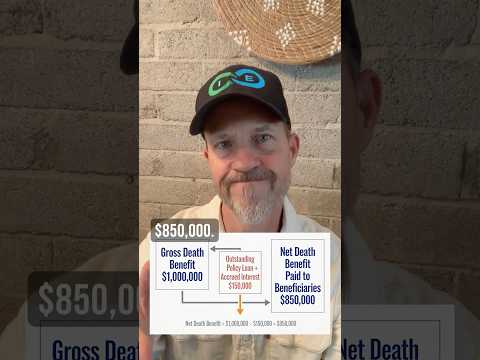

• Simple numbers on screen: “Death benefit: $1,000,000;

Loan: $150,000;

Net to heirs: $850,000.”

Where people get hurt is not the existence of policy loans; it’s misuse and neglect.

If you borrow heavily and never pay attention, the interest can grow, the loan can approach the cash value, and the policy can eventually lapse.

If that happens, the policy terminates, the coverage disappears, and in many cases there can be a tax bill because the IRS may treat that gain as if you cashed the policy out.

From an estate attorney’s chair, that’s my nightmare scenario: the client thought they had a tax‑advantaged asset for their family, and instead they end up with no coverage and a surprise tax problem.”

Used wisely, policy loans can be a very elegant estate and cash‑flow tool.

You can access capital for opportunities, emergencies, or even to equalize inheritances among children, while keeping the policy in force and the long‑term death benefit intact.

The key is treating it like a real banking system: track your loans, set up a repayment plan when appropriate, and have your insurance professional and your estate attorney on the same page.

“Control this amazing tool → Don’t let it control you.”

Grab a copy of the self banking blue print to find out how I became so passionate about this asset as a practicing trusts and estates attorney.

There is a ton of confusion around policy loans in whole life insurance. People are told, ‘You’re borrowing your own money,’ or ‘The insurance company will steal your cash value.’

Let’s cut through the sales talk and look at what’s actually happening in the contract, and what it means for your family and your estate.”

Disclaimer:

“This Is Not Legal Advice, For Education Only”

First, a policy loan is not a personal IOU or borrowing your own cash.

It’s a loan from the insurance company, with your policy’s cash value as collateral.

Think of your cash value as the equity in a house. You don’t rip the bricks out of the house to get money; you borrow against the equity, and the house stays standing.

Same idea here: your cash value stays in the policy, continues to earn its guaranteed growth and potential dividends, and the company advances you their money, secured by that cash value.

Now, the part most people never hear clearly: interest and collateral.

When you take a policy loan, the insurance company charges a stated interest rate. That interest doesn’t come out of thin air; it accrues on the loan balance, just like any other loan.

If you never repay it during your lifetime, the company doesn’t chase your kids. They simply subtract the outstanding loan plus interest from your death benefit before it’s paid to your beneficiaries.

From an estate planning perspective, that means two things:

1. You’re effectively choosing to ‘repay’ the loan with a reduced death benefit if you don’t repay it during life.

2. As long as the policy is monitored and doesn’t lapse, your heirs still receive what’s left—net of the loan—without going through probate.”

Visuals:

• Simple numbers on screen: “Death benefit: $1,000,000;

Loan: $150,000;

Net to heirs: $850,000.”

Where people get hurt is not the existence of policy loans; it’s misuse and neglect.

If you borrow heavily and never pay attention, the interest can grow, the loan can approach the cash value, and the policy can eventually lapse.

If that happens, the policy terminates, the coverage disappears, and in many cases there can be a tax bill because the IRS may treat that gain as if you cashed the policy out.

From an estate attorney’s chair, that’s my nightmare scenario: the client thought they had a tax‑advantaged asset for their family, and instead they end up with no coverage and a surprise tax problem.”

Used wisely, policy loans can be a very elegant estate and cash‑flow tool.

You can access capital for opportunities, emergencies, or even to equalize inheritances among children, while keeping the policy in force and the long‑term death benefit intact.

The key is treating it like a real banking system: track your loans, set up a repayment plan when appropriate, and have your insurance professional and your estate attorney on the same page.

“Control this amazing tool → Don’t let it control you.”

Grab a copy of the self banking blue print to find out how I became so passionate about this asset as a practicing trusts and estates attorney.

- Категория

- Кредит под залог

Комментариев нет.

Следующее

-

40:02

Policy Loans vs Traditional Loans | Why Banks Hate This Strategy #infinitebanking

-

00:16

Policy Loans Explained — Use Your Life Insurance Like a Personal Bank

-

01:03

Policy Loans at Death — This Question Catches Students Every Time

-

01:06

How I used Whole Life Insurance Policy Loans to support my family

-

01:49

Taking Loans for Crypto? Here’s the Truth No One Tells You

-

02:11

How The Rich Actually Live On Loans (The Truth No One Tells You)

-

00:32

Secret Hack To Get Real Estate Loans

-

02:04

What is TILA (Truth in Lending Act)? | REAL-ESTATE-SALESPERSON Exam Prep

-

02:37

Infinite Banking Explained — By An Estate Attorney #infinitebanking

-

01:02

He Spent the Money and Still Earned on All of It (How Policy Loans Work) #shorts

-

03:11

Что делать, если банк продал долг или кредит коллекторам 2019?

-

10:34

Кредитная карта зло 2019? Кредиты от Тинькофф , Сбербанка, альфа банка и других

-

02:15

Как оплатить кредит Почта Банка через Сбербанк Онлайн

-

06:03

Оплата кредита другого банка через мобильное приложение СБЕРБАНК ОНЛАЙН

-

04:15

Спрашиваем лицензию на кредитование у банка Хоум Кредит

-

08:52

Почта Банк: как пользоваться приложением

-

03:39

Евразийский Банк кредит қалай төлейді

-

14:40

Как я попал в ДОЛГОВУЮ ЯМУ: опасные кредиты, банки и долги

-

08:19

ОПРОС: В каком банке взять кредит?

-

02:45

Как оформить кредит без посещения отделений? | Идея Банк